You know that feeling when your business is growing, orders are coming in, but you're staring at a stack of unpaid invoices while payroll is due next week? You're definitely not alone. With traditional banks and SBA lenders tightening their requirements in 2025, more business owners are discovering that alternative funding solutions might actually be better fits for their cash flow needs.

The good news is that you have options, and some of them can get money in your account faster than you might think. Let's break down three popular cash flow solutions so you can figure out which one makes sense for your situation.

The Current Funding Landscape (And Why Alternatives Matter More Than Ever)

Before we dive into your options, here's what's happening in the lending world right now. Traditional banks have gotten pickier about who they'll lend to, requiring higher credit scores and more paperwork than ever. The SBA loan process, while still valuable, can take months, and recent government delays have frozen billions in approvals, leaving business owners in limbo.

This shift has created a huge opportunity for alternative funding solutions. These aren't your grandfather's business loans, but they're often exactly what modern businesses need: fast, flexible, and focused on your actual business performance rather than just your credit score.

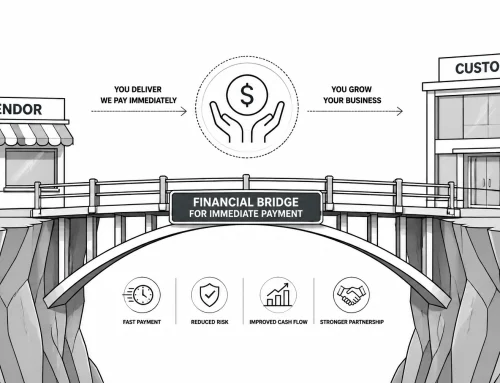

Invoice Factoring: Turn Your Invoices Into Immediate Cash

Think of invoice factoring as selling your unpaid invoices to get cash today instead of waiting 30, 60, or 90 days for customers to pay. Here's how it works: a factoring company buys your invoices at a discount (usually 80-95% of face value), gives you cash immediately, then collects payment directly from your customers.

The Upside of Invoice Factoring

The biggest advantage? Speed. Most factoring companies can approve you and get cash in your account within 24-48 hours. And here's something that surprises many business owners, factoring doesn't create debt on your balance sheet. You're not borrowing money; you're selling an asset.

The approval process is also more forgiving than traditional loans. Factoring companies care more about whether your customers will pay than whether you have perfect credit. This makes it a lifeline for newer businesses or those going through rough patches.

The Reality Check

Let's be honest about the costs. Factoring fees typically run 0.5% to 3.75% per invoice, plus various processing fees that can add up quickly. If you're factoring $10,000 worth of invoices monthly, you could easily pay $300-500 per month in fees.

There's also the customer relationship factor to consider. Your customers will know you're factoring because they'll be sending payments to the factoring company. Some might see this as a sign of financial trouble (even though it's not), and you'll want to manage that perception carefully.

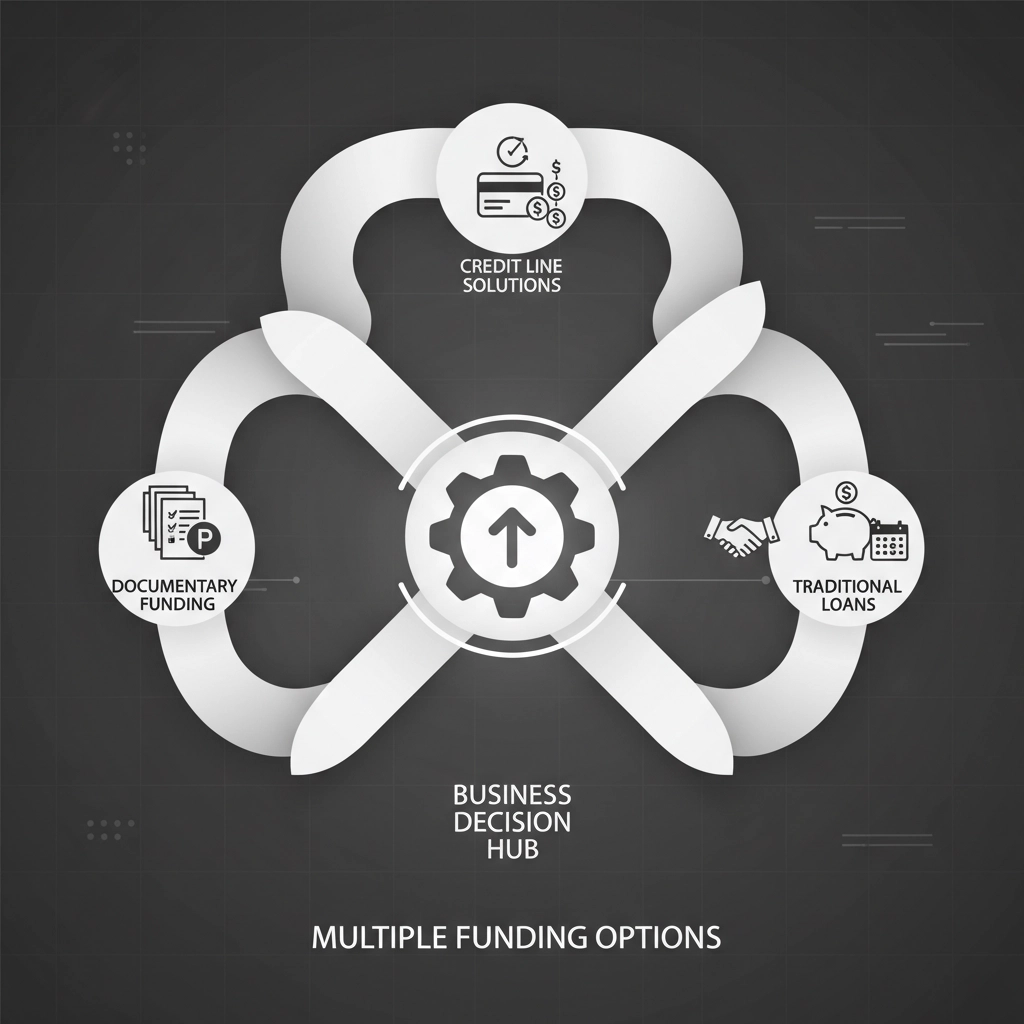

AR Financing: A More Traditional Approach to Invoice-Based Funding

Accounts receivable financing works like a credit line secured by your unpaid invoices. Instead of selling individual invoices, you use your entire book of receivables as collateral for ongoing access to funds.

How AR Financing Differs

The fee structure is where AR financing really differs from factoring. Instead of paying per invoice, you typically pay a fixed monthly fee regardless of how much you use. This can make budgeting easier and might save money if you consistently need access to funds.

You also maintain more control over customer relationships since you're still handling collections. The financing company is more like a silent partner providing credit against your receivables.

The Trade-offs

AR financing usually requires stronger credit than factoring, and the approval process can be more rigorous. You'll need a solid track record of receivables and customers with good payment histories. Think of it as the middle ground between factoring and traditional loans, more requirements than factoring, but more flexibility than bank loans.

Working Capital Loans: The Traditional Route With Modern Twists

Working capital loans are exactly what they sound like, traditional loans designed to fund your day-to-day operations. You get a lump sum upfront and repay it with interest over time.

Why Working Capital Loans Still Make Sense

The main advantage is control. Once you have the money, you can use it however your business needs, payroll, inventory, equipment, marketing, or just keeping cash reserves healthy. You're not limited to invoice-related uses like you are with factoring or AR financing.

Interest rates can also be more predictable than factoring fees, especially if you have good credit. And unlike factoring, your customers never know you've borrowed money.

The Requirements Reality

Here's the catch: working capital loans typically require the strongest credit and most documentation. Lenders want to see established businesses with predictable cash flows and solid financials. If you're a newer business or going through challenges, this might not be your best option right now.

The Side-by-Side Comparison

| Factor | Invoice Factoring | AR Financing | Working Capital Loan |

|---|---|---|---|

| Speed to funds | 24-48 hours | 2-7 days | 1-4 weeks |

| Credit requirements | Most flexible | Moderate | Strictest |

| Creates debt? | No | No | Yes |

| Customer involvement | Direct (they pay factor) | Minimal | None |

| Cost structure | Per-invoice fees | Fixed monthly fee | Interest + payments |

| Use flexibility | Invoice-related only | Invoice-related only | Any business purpose |

| Best for | Quick cash, poor credit | Consistent invoice flow | Established businesses |

Which Solution Fits Your Business?

Choose Invoice Factoring If:

You need cash immediately and have customers who pay invoices reliably (even if slowly). This works especially well if you're a service business, distributor, or manufacturer with B2B customers on net-30 or longer terms. Don't worry if your personal credit isn't perfect, factoring companies focus on your customers' creditworthiness more than yours.

Choose AR Financing If:

You consistently generate large invoices and need ongoing access to working capital rather than one-time cash infusions. This makes sense if you have seasonal fluctuations or project-based income cycles. You'll need decent business credit, but the fixed fee structure can save money if you use the facility regularly.

Choose Working Capital Loans If:

You have strong credit, need maximum flexibility in how you use funds, and want predictable repayment terms. This is often the best choice for established businesses looking to invest in growth opportunities or maintain cash reserves for strategic purposes.

Making the Right Choice for Your Situation

Here's the thing: there's no universally "best" option. The right funding solution depends on your specific situation, timeline, and goals. Some businesses even use multiple solutions at different times or for different purposes.

If you're still unsure, consider starting with the option that has the lowest barrier to entry for your situation. You can always explore other alternatives as your business grows and your needs change.

Remember, these funding solutions exist to help your business thrive, not just survive. The goal isn't just to solve today's cash flow challenge, it's to set yourself up for sustainable growth. Sometimes that means choosing the slightly more expensive option that gives you better control, or the more restrictive option that costs less in the long run.

Don't let perfect be the enemy of good when it comes to business funding solutions. The best choice is often the one that gets you the cash flow you need to keep moving forward, serve your customers, and capture the opportunities in front of you.

At HUB Funding Solutions, we've helped hundreds of businesses navigate these exact decisions. Every situation is unique, and sometimes the right answer becomes clear once you talk through your specific needs with someone who understands the full landscape of funding solutions available today.

The key is taking action rather than letting cash flow challenges hold your business back from its potential.