January 2026 is coming in hot, and it's bringing three pay periods with it instead of the usual two. If you're feeling that familiar knot in your stomach thinking about cash flow, you're definitely not alone. This calendar quirk happens every few years, and it catches even the most prepared business owners off guard.

While you can't control the calendar, you absolutely can control how you respond to it. Smart business owners are already thinking ahead, and payroll financing might just be the secret weapon you need to not just survive January, but actually use it as a launching pad to dominate the entire first quarter.

Why January's Triple Payroll Hits Different

Let's be real about what we're dealing with here. Most months, you've got a predictable payroll rhythm. You know exactly when those expenses are hitting, and you can plan accordingly. But January 2026? It's like your cash flow got ambushed.

Whether you pay weekly or bi-weekly, you're looking at payroll dates falling on January 3rd, 10th, 17th, 24th, and 31st. That's potentially three full payroll cycles in a single month, a 50% increase in your normal payroll expenses right when you're trying to recover from holiday slowdowns and get back into business mode.

And it's not just about the money leaving your account. It's about timing. Your customers might still be slow to pay invoices from December, but your employees (rightfully) expect their paychecks on schedule. That gap between when you need to pay out and when money flows back in? That's where things get interesting.

The Hidden Opportunity in Cash Flow Challenges

Here's what most business owners miss: cash flow challenges aren't just problems to solve, they're opportunities to level up your financial strategy. When you handle January's payroll crunch smartly, you're not just keeping the lights on. You're positioning yourself to take advantage of Q1 opportunities that your less-prepared competitors will have to pass up.

Think about it. While other businesses are scrambling to cover basic expenses or delaying growth investments because they're cash-strapped from January's payroll hit, you could be:

- Securing new contracts that require upfront investment

- Taking advantage of early-year equipment deals

- Hiring that key team member you've been wanting to add

- Building inventory for spring demand

The difference? Having reliable access to working capital when you need it most.

Strategy 1: Bridge the Invoice-to-Payment Gap

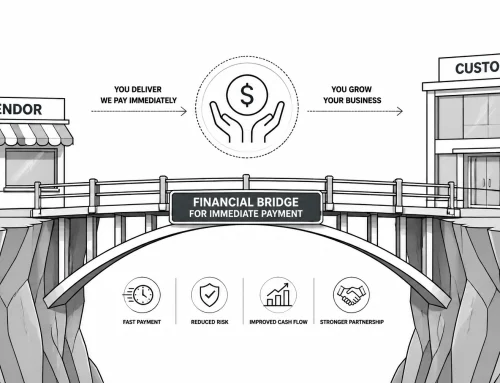

Payroll financing works differently than traditional loans, and that's exactly why it's so powerful for managing irregular cash flow periods. Instead of borrowing against future earnings or putting up collateral, you're essentially getting paid faster for work you've already completed.

Here's how it typically works: You submit your outstanding invoices, and within 24 hours (sometimes the same day), you can access a percentage of those funds, usually 80-90%. Your customers still pay the invoices normally, but instead of waiting 30, 60, or 90 days to get paid, you get the cash flow you need right now.

This is particularly powerful in January because you're likely carrying receivables from December work. Rather than waiting for those payments to trickle in while you're hitting three payroll cycles, you can access that money immediately. It's not debt, it's simply accelerating your own income.

Strategy 2: Scale Funding to Match Your Actual Needs

One of the biggest mistakes businesses make is either over-borrowing (and paying unnecessary fees) or under-borrowing (and still running into cash flow problems). Payroll financing offers something traditional loans can't: the ability to scale your funding to match your exact needs.

Need to cover $15,000 in extra payroll for January? You can access exactly that amount based on your invoices. Business picking up and February looking heavy too? You can access more. Things stabilizing in March? You naturally access less as you need less.

This flexibility means you're not locked into fixed monthly payments that don't match your business's natural rhythm. Instead, you're paying for funding only when you're actually using it, and the repayment comes directly from the invoices you've already generated.

Strategy 3: Keep Your Operating Capital Free for Growth

This might be the most important strategy of all. When you use payroll financing to handle January's cash flow challenge, you're preserving your operating capital for the opportunities that define a successful Q1.

Think about what happens when you drain your cash reserves to cover payroll. Sure, your employees get paid (which is obviously critical), but now you're operating on empty. When that perfect client calls with a project that requires some upfront investment, or when you spot equipment that could transform your efficiency, you're stuck saying "maybe next quarter."

But when you've handled payroll through financing, your operating capital stays intact. You can say yes to opportunities. You can invest in growth. You can act like the successful, forward-thinking business owner you are, instead of someone just trying to keep the doors open.

Beyond Payroll: Equipment and Fleet Financing for Q1 Growth

While we're talking about positioning yourself for Q1 success, it's worth considering how equipment financing can complement your payroll strategy. Many of our clients find that once they've solved their immediate cash flow challenges, they're in a perfect position to upgrade equipment or expand their fleet capabilities.

Whether it's construction equipment to handle spring contracts, delivery vehicles to support growing e-commerce operations, or technology upgrades to improve efficiency, having access to equipment financing means January's payroll challenge doesn't derail your growth plans. We work with dealer partnerships throughout regions like Dallas and beyond, making it easier to secure both the equipment and the financing in one smooth process.

Vehicle financing, in particular, can be a game-changer for businesses looking to expand their service area or improve their professional image in Q1. From work trucks to delivery vans to executive vehicles, having reliable transportation financing options means you can grow your business capabilities while managing your cash flow responsibly.

The Peace of Mind Factor

Let's talk about something that doesn't show up on financial statements but absolutely affects your bottom line: peace of mind. When you know you can handle unexpected cash flow challenges, you make better business decisions. You're not operating from a place of financial stress, which means you can focus on growth, strategy, and serving your customers better.

Getting Started: What You Need to Know

If you're thinking payroll financing might be right for your business, here's what the process typically looks like. Most providers will want to see your recent invoices, understand your payment terms with customers, and get a sense of your business's track record. The good news? If you're generating invoices regularly and your customers have a decent payment history, you're probably already qualified.

The application process is usually straightforward: much simpler than traditional business loans. You're not putting your personal assets at risk, and there's no long-term debt obligation. You're simply accessing your own money faster.

Most businesses can get approved and funded within 24-48 hours, which means even if January caught you off guard this year, you could still get ahead of the cash flow challenge.

Your Next Steps

Don't wait until you're staring at payroll due dates to start exploring your options. The businesses that dominate Q1 are the ones that plan ahead, and that planning starts now.

Remember, you've built a business that generates invoices and serves customers. That's already proof that you have what it takes to succeed. Sometimes you just need the right financial tools to make sure cash flow timing doesn't get in the way of that success.

Click here to apply: https://tinyurl.com/3deu6mpe