Picture this: You're running a successful manufacturing business, orders are coming in steadily, and your production line is humming along nicely. But when you look at your bank account, you're wondering where all that money went. Sound familiar? You're not alone, and more importantly, you're not stuck.

The culprit behind this cash flow mystery often lies in something called the cash conversion cycle. Don't worry, it's not as complicated as it sounds, and understanding it could literally put tens of thousands of dollars back into your business's pocket.

What Exactly Is the Cash Conversion Cycle?

Think of the cash conversion cycle as the journey your money takes from the moment you buy raw materials until you finally get paid by your customers. It's like a financial relay race where your cash gets passed from station-to-station. It goes through raw materials, work-in-progress, finished goods, and accounts receivable before it finally makes it back home to your bank account.

For manufacturers, this journey can be particularly long. You might order steel in January, turn it into products in February, ship them in March, and not get paid until April. That's a lot of time for your cash to be tied up doing laps around your business instead of helping you grow.

The good news? Every day you can shave off this cycle puts money back in your pocket faster.

The Three Moving Parts of Your Cash Conversion Cycle

Your cash conversion cycle has three main components, and understanding each one gives you the power to make meaningful changes:

Days Inventory Outstanding (DIO)

This measures how long your raw materials and finished products sit around before they're sold. Think of DIO as the "sitting around time" for your inventory.

If you're holding $100,000 worth of inventory and your monthly cost of goods sold is $50,000, your inventory is sitting for about 60 days on average. That's 60 days where your cash is basically taking a nap instead of working for you.

Days Sales Outstanding (DSO)

DSO tracks how long it takes customers to actually pay you after you've delivered their orders. We've all been there, you complete a big job, send the invoice, and then wait… and wait… and wait.

Some customers pay in 15 days, others take 60. Your DSO is the average across all your customers, and it directly impacts how quickly you can reinvest in your business.

Days Payable Outstanding (DPO)

This one's actually working in your favor, it's how long you take to pay your suppliers. The longer you can reasonably extend this (without damaging relationships), the longer you keep cash in your business to fund operations.

The Magic Formula

Here's where it gets interesting: Cash Conversion Cycle = DIO + DSO – DPO

Let's say your inventory sits for 45 days (DIO), customers pay in 30 days (DSO), and you pay suppliers in 25 days (DPO). Your cash conversion cycle would be 45 + 30 – 25 = 50 days.

This means for 50 days, your working capital is tied up in operations. If your monthly revenue is $200,000, that's about $83,000 tied up for almost two months. Reduce that cycle by just 15 days, and you've freed up about $25,000 in working capital.

Why Manufacturers Feel the Squeeze More Than Others

Manufacturing businesses face unique challenges that make cash flow management crucial. Unlike a software company that can deliver a product instantly, you're dealing with physical materials, production time, shipping, and often complex supply chains.

Your cash gets locked up at multiple stages when you buy raw materials during production (paying for labor and overhead), while products sit in finished goods inventory, and during the collection process. Each stage extends the time before you see that money again.

But here's the encouraging part: because manufacturing has more moving parts, you also have more opportunities to make improvements that create real impact.

Calculating Your Current Cycle (Don't Worry, It's Easier Than You Think)

You don't need to be a financial wizard to figure this out. Grab your most recent financial statements and let's walk through this together.

Step 1: Find Your DIO

Take your average inventory value and divide it by your daily cost of goods sold. If your average inventory is $75,000 and your annual COGS is $900,000, your daily COGS is about $2,466. Your DIO would be $75,000 ÷ $2,466 = about 30 days.

Step 2: Calculate Your DSO

Divide your accounts receivable by your daily credit sales. If you have $40,000 in receivables and daily sales of $1,500, your DSO is about 27 days.

Step 3: Determine Your DPO

Divide your accounts payable by your daily purchases. If you owe suppliers $25,000 and make daily purchases of $1,200, your DPO is about 21 days.

Step 4: Put It All Together

30 (DIO) + 27 (DSO) – 21 (DPO) = 36 days

In this example, your cash is tied up for 36 days in each cycle.

Practical Strategies to Free Up Your Working Capital

Now for the fun part, actually improving your cash conversion cycle. Small changes in each area can add up to significant cash flow improvements.

Speed Up Your Inventory Game

Look at your inventory with fresh eyes. Are you holding onto slow-moving items "just in case"? Consider implementing just-in-time ordering for your most predictable materials.

One manufacturing client reduced their DIO from 60 days to 45 days simply by analyzing their inventory patterns and being more strategic about reorder points. That 15-day improvement freed up $35,000 in working capital.

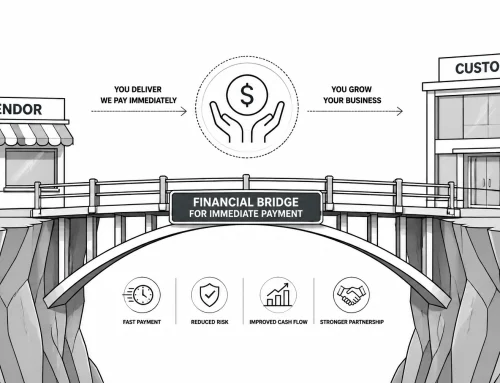

Looking for a quick win on inventory? HUB Funding Solutions can tailor financing equipment, financing/leasing, working capital loans, AR finance, invoice factoring, and project finance, so you stock what you need without squeezing cash. Let's connect for a plan tuned to your production schedule.

Get Paid Faster (Without Annoying Your Customers)

Offer small discounts for early payment: even 1-2% can motivate customers to pay within 10 days instead of 30. Improve your invoicing process by sending invoices immediately upon delivery, not at month-end.

Consider requiring deposits on large orders or shorter payment terms for new customers. Most customers understand these are standard business practices.

Want cash in the door sooner? HUB Funding Solutions can customize AR finance and invoice factoring to turn receivables into immediate cash, and pair them with working capital loans or equipment financing to smooth production and delivery. Talk with us for a receivables plan that fits your customers and terms.

Negotiate Smarter with Suppliers

Don't be afraid to ask suppliers for extended payment terms, especially if you're a reliable customer. Many suppliers would rather have consistent, slightly delayed payments than deal with the uncertainty of new customers.

Just remember, this isn't about taking advantage. It's about creating mutually beneficial relationships that help your cash flow while maintaining good supplier partnerships.

Need more breathing room on payables? HUB Funding Solutions can customize solutions, project finance, working capital loans, equipment financing/leasing, AR finance, and invoice factoring, so you can extend terms, capture early-pay discounts, and keep cash moving. Let's talk through the right mix for your vendor strategy.

Real-World Impact: What This Means for Your Bottom Line

Let's put this in perspective with a real example. Imagine you're running a $2 million annual revenue manufacturing business. Your current cash conversion cycle is 75 days, which means you have about $410,000 tied up in working capital at any given time.

By implementing the strategies above, you reduce your cycle to 50 days, a very achievable goal. That frees up approximately $137,000 in working capital. That's money you can use to invest in new equipment, hire additional staff, or simply sleep better knowing you have a stronger cash cushion.

Monitoring Your Progress (Because What Gets Measured Gets Improved)

Don't just calculate your cash conversion cycle once and forget about it. Track it monthly or quarterly to spot trends and celebrate improvements. Even small reductions compound over time.

Create a simple dashboard that shows your DIO, DSO, DPO, and overall cycle. When you see the numbers improving month over month, you'll know your efforts are paying off, literally.

Making It Sustainable

The most successful manufacturers treat cash conversion cycle management as an ongoing process, not a one-time fix. Regular supplier negotiations, continuous inventory optimization, and proactive customer collection practices become part of their business rhythm.

Remember, you don't have to tackle everything at once. Pick one area, maybe starting with accounts receivable since that's often the quickest win, and focus on making consistent improvements there before moving to the next area.

Your manufacturing business has unique cash flow challenges, but it also has tremendous opportunities for improvement. By understanding and optimizing your cash conversion cycle, you're not just freeing up working capital: you're creating a more resilient, flexible business that can weather unexpected challenges and capitalize on growth opportunities.

The journey to better cash flow starts with understanding where your money goes and how long it takes to come back. From there, every improvement you make puts you in a stronger position to grow and succeed. And if you need support along the way, remember that HUB Funding Solutions is here to help you navigate these challenges and unlock your business's full potential.

Your cash conversion cycle doesn't have to be a mystery anymore, it can be your roadmap to better cash flow and stronger business growth.